병장 월급 150만원 시대… '軍 테크'로 목돈 모아보자 Military Personnel Target Lump Sum Savings

작성자정승남세기영어교육연구회장작성시간26.06.22조회수89 목록 댓글 0병장 월급 150만원 시대… '軍 테크'로 목돈 모아보자

Military Personnel Target Lump Sum Savings with High-Interest Products

병사 전용 금융 상품 잇따라

Specialized savings offer up to 10% interest; Patriot Card discounts aid expense reduction

전문 저축은 최대 10%의 이자를 제공하며, 패트리어트 카드는 지원 비용 절감을 할인합니다

유소연 기자 입력 2026.06.22. 00:37 조선일보

최근 입대한 A(20)씨는 이병 월급 75만원 중 70%가 넘는 55만원을 매달 적금에 넣고 있다. 그는 제대할 때쯤 목돈으로 최소 2000만원을 만드는 게 목표다. A씨는 “주변에 주식 투자하는 친구들도 많은데, 원금을 건드리지 않고 고금리를 얹어주는 군인 대상 금융 상품이 훨씬 안정적이라고 생각했다”며 “진급 후 월급이 늘면 매달 붓는 적금액을 더 늘릴 계획”이라고 했다.

그래픽=박상훈

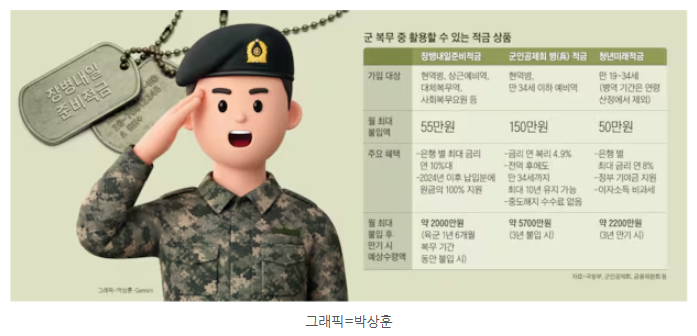

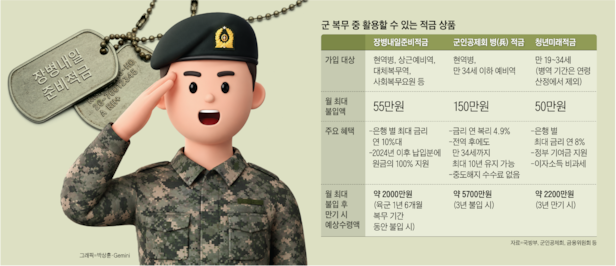

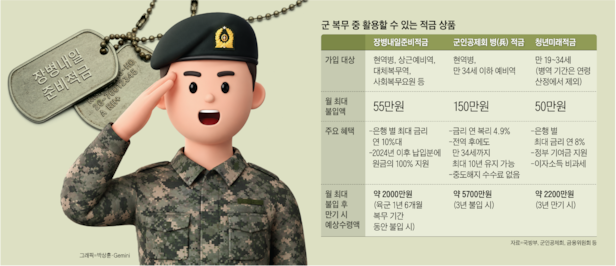

◇전역 때 2000만원, 장병내일준비적금

병사 월급이 과거보다 늘면서 A씨처럼 저축 등 재테크에 관심을 갖고 복무 기간 중 목돈을 만들려는 현역병이 많아지고 있다. 올해 계급별 기본급은 이병이 월 75만원, 일병 90만원, 상병 120만원, 병장 150만원 등이다.

특히 군인 대상 정책 금융 상품은 원금을 지키면서도 높은 금리를 제공하는 경우가 많고, 군 생활 중 생활비가 크게 들지 않는 만큼 ‘군(軍)테크’에 나서 목돈 마련을 계획하는 것이다.

2018년 마련된 장병내일준비적금이 대표적이다. 현역병 등을 대상으로 한 이 상품은 은행에 따라 최고 연 10%대 금리를 제공한다. 현재 하나은행이 최고 연 10.1%, KB국민은행과 신한은행이 연 10%, IBK기업은행이 연 9.7%, NH농협은행이 연 7.5% 금리를 제공하고 있다.

이 상품은 은행별로 최대 월 30만원까지 납입할 수 있고, 1인당 최대 2개 계좌를 만들 수 있다. 계좌 2개를 만들면 합쳐서 월 최대 55만원까지 납입할 수 있다.

만약 복무 기간 18개월간 매달 55만원을 채워서 넣으면 정부 기여금과 이자를 합쳐 전역할 때쯤 2000만원 넘는 목돈이 생긴다. 만기일은 전역 예정일이다. 전역 후 추가 납입은 불가하다.

◇전역 후 유지, 군인공제회 저축

계급이 올라 월급이 오른다면 현역 복무 중 가입하면 전역 이후에도 계속 유지할 수 있는 군인공제회 ‘병(兵) 회원 저축’을 추가해도 좋다. 이 상품은 연 4.9% 복리 이자가 적용된다. 월 150만원까지 불입할 수 있고 전역 후에도 최대 10년(만 34세까지) 유지 가능하다. 중도 해지 수수료도 없다.

만약 월 150만원을 채워 10년간 유지한다면 원금은 1억8000만원이며, 이자까지 합쳐 세후 2억2000만원을 모을 수 있다. 월 30만원씩 5년만 납입해도 만기 시 세후 2000여 만원이 생긴다.

이 상품은 무엇보다 현역 시절 가입 이력이 있어야 전역 후에도 혜택을 이어갈 수 있다는 점을 유의해야 한다. 즉, 전역 전 가입해 월 1만원이라도 납입해 놓는 게 좋다. 이후 취업해 소득이 늘어난다면 월 불입액을 늘리는 것도 방법이다.

◇청년미래적금도 가입 가능

22일부터 만 19~34세 청년을 대상으로 가입 신청을 받기 시작하는 청년미래적금도 군대에서 가입할 수 있다. 장병내일준비적금과 중복 가입도 가능해 두 상품을 모두 가입하면 수천만 원대 목돈 마련이 가능하다.

청년미래적금은 기본 금리 연 5%에 은행별 우대 금리 2~3%포인트가 더해져 연 7~8% 수준의 금리를 제공한다. 최대 불입액인 월 50만원씩 3년을 채워 납입한다면 정부 기여금을 합쳐 약 2200만원을 만들 수 있다.

지난 19일 기준 은행연합회 공시에 따르면, KB국민·신한·하나·우리·NH농협·IBK기업은행과 우체국이 최고 연 8% 금리를 준다. 다만 이 상품도 장병내일준비적금처럼 은행마다 급여 이체, 카드 이용, 재무 상담 등 우대 금리 조건이 붙는다.

참고로 이 상품은 나이 제한이 있지만 병역 기간은 연령 산정에서 최대 6년까지 빼준다. 즉 현재 만 35세라도 2년간 병역을 했다면 33세로 간주돼 가입할 수 있다.

◇나라사랑카드로 생활비 아끼기

이미 쓰고 있는 나라사랑카드가 있다면, 앞선 적금 상품들의 우대 금리 조건에 카드 이용 실적 등이 있는지 살펴보고 해당 은행에 가입하는 것도 방법이다.

나라사랑카드는 병역 의무자를 대상으로 발급되는 체크카드인데, 일반 카드보다 혜택이 많고 전역 후에도 쓸 수 있어 인기가 많다. 올해부터는 신한·하나·IBK기업은행에서 나라사랑카드 사업을 맡고 있다.

대중교통비가 20% 할인되는 데다가 군마트(PX)에서 하나·IBK기업은행은 최대 30%, 신한은행은 20% 할인해 준다. 편의점에서는 신한은행은 GS25·CU에서 20%, IBK기업은행은 GS25·CU·이마트24에서 10% 할인해 준다. 하나은행은 CU 행사 품목에 대해 10% 할인 혜택을 준다.

2013년부터 기자 생활을 시작해 경제부에서 가장 오래 일하고 있다. 국제경제 섹션인 ‘위클리비즈’팀과 재테크팀을 거쳐 현재 금융시장팀에서 한국은행 및 시중은행, 보험, 여신 업계 등을 취재하고 있다. 저서로 <합정과 망원 사이>, <차마 하지 못했던 말>이 있다.

-----------------------------------------------------------------------------------------------------------------------------------------

Military Personnel Target Lump Sum Savings with High-Interest Products

Specialized savings offer up to 10% interest; Patriot Card discounts aid expense reduction

| By You So-yeon Published 2026.06.22. 00:37 The Chosun Daily Newspaper / 조선일보 A (20), a recent enlistee, deposits over 70% of his monthly private first class salary of 750,000 Korean won—550,000 Korean won—into a savings account each month. His goal is to accumulate at least 20 million Korean won by the time he is discharged. A said, “Many of my peers are investing in stocks, but I thought military-targeted financial products that offer high interest rates without touching the principal were much more stable. ‘After promotion, when my salary increases, I plan to increase my monthly savings amount,’” he added.  ◇20 million Korean won at Discharge: Military Personnel Tomorrow Preparation Savings As soldiers’ salaries have increased compared to the past, more active-duty personnel like A are focusing on financial planning, such as savings, to build a lump sum during their service. This year, the basic monthly pay by rank is 750,000 Korean won for private first class, 900,000 Korean won for private, 1.2 million Korean won for corporal, and 1.5 million Korean won for sergeant. Policy financial products for military personnel often guarantee principal protection while offering high interest rates. Since living expenses during military service are not significant, many soldiers engage in “military tech” to prepare for a lump-sum fund. The Military Personnel Tomorrow Preparation Savings, established in 2018, is a representative product. Targeting active-duty soldiers, it offers annual interest rates of up to 10% depending on the bank. Currently, Hana Bank provides 10.1%, KB Kookmin Bank and Shinhan Bank offer 10%, Industrial Bank of Korea (IBK) provides 9.7%, and NH Nonghyup Bank offers 7.5%. This product allows monthly deposits of up to 300,000 Korean won per bank, with individuals able to open up to two accounts. By creating two accounts, soldiers can deposit a maximum of 550,000 Korean won monthly. If 550,000 Korean won is deposited monthly for 18 months during service, the total, including government contributions and interest, will exceed 20 million Korean won by discharge. The maturity date aligns with the discharge date, and additional deposits after discharge are not allowed. ◇Post-Discharge Savings: Military Personnel Credit Union Savings If a soldier’s rank increases and salary rises, they can additionally join the Military Personnel Credit Union’s “Enlisted Member Savings,” which can be maintained even after discharge. This product applies a 4.9% annual compound interest rate. Monthly deposits of up to 1.5 million Korean won are allowed, and the account can be maintained for up to 10 years (until age 34) after discharge. There are no early termination fees. If 1.5 million Korean won is deposited monthly for 10 years, the principal amounts to 180 million Korean won, and with interest, it totals 220 million Korean won after tax. Even depositing 300,000 Korean won monthly for five years results in 20 million Korean won after tax at maturity. This product requires enrollment during active duty to continue benefits after discharge. It is advisable to deposit at least 10,000 Korean won monthly before discharge. After employment and increased income, increasing monthly deposits is an option. ◇Youth Future Savings Also Available Starting from the 22nd, the Youth Future Savings, open to youths aged 19–34, can be joined by military personnel. It can be subscribed to simultaneously with the Military Personnel Tomorrow Preparation Savings, enabling the accumulation of tens of millions of Korean won. The Youth Future Savings offers a base interest rate of 5% annually, with bank-specific preferential rates of 2–3 percentage points, resulting in 7–8% annual rates. Depositing the maximum 500,000 Korean won monthly for three years, including government contributions, can yield approximately 22 million Korean won. As of the 19th, according to the Bankers’ Association of Korea, KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup, Industrial Bank of Korea (IBK), and the Post Office offer up to 8% annual interest. However, like the Military Personnel Tomorrow Preparation Savings, preferential rates require conditions such as salary transfers, card usage, or financial counseling. Note that while this product has an age limit, military service periods can deduct up to six years from age calculations. For example, a 35-year-old who served for two years is considered 33 and eligible. ◇Saving on Living Expenses with the Patriot Card If using the existing Patriot Card, check if preferential interest conditions for the aforementioned savings products include card usage. The Patriot Card, a check card issued for military personnel, offers more benefits than regular cards and remains usable after discharge. Since this year, Shinhan, Hana, and Industrial Bank of Korea (IBK) have managed the Patriot Card business. Public transportation fares are discounted by 20%, and military marts (PX) offer up to 30% discounts at Hana and Industrial Bank of Korea (IBK), and 20% at Shinhan Bank. At convenience stores, Shinhan Bank provides 20% discounts at GS25 and CU, while Industrial Bank of Korea (IBK) offers 10% at GS25, CU, and Emart24. Hana Bank gives a 10% discount on CU promotional items. · This article has been translated by Upstage Solar AI. |

21세기 영어교육연구회 / ㈜ 파우스트 칼리지

Phone : (02)386-4802 / (02)384-3348

E-mail : faustcollege@naver.com / ceta211@naver.com

Twitter : http://twitter.com/ceta21 21세기 영어교육연구회

Web-site : www.faustcollege.com (주)파우스트 칼리지

Cafe : http://cafe.daum.net/21ceta 21세기 영어교육연구회

Band : http://band.us/@ceta21 21세기 영어교육연구회

Blog : http://blog.naver.com/ceta211 21세기 영어교육연구회