Expected BOK rate hike prompts concern 한은의 금리인상예상으로 가계와 기업의 금리부담 가중우려

작성자Condel작성시간26.06.08조회수74 목록 댓글 0

한국은행의 금리 인상 전망이 가계와 기업의 부담을 가중시키고 있습니다.

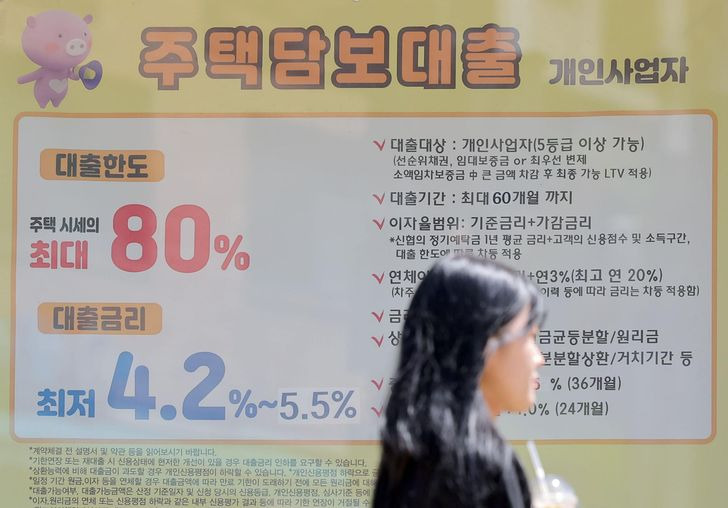

주요 은행의 고정형 주택담보대출 금리가 7.33%까지 상승하며 2022년 10월 이후 최고치를 기록했습니다.

주식시장 상승과 함께 증가한 마진대출은 금리상승 시 반대매매 위험을 높이며 시장 변동성을 키울 수 있습니다.

인플레이션 억제를 위한 금리인상이 불가피하더라도, 경기둔화 및 금융 취약계층 부담을 고려한 신중한 정책 운용이 요구됩니다.

Expected BOK rate hike prompts concern over rising interest burdens on households, firms

한은의 금리인상예상으로 가계와 기업의 금리부담 가중우려

By Lee Hyo-jin이효진 기자

Published Jun 7, 2026 3:17 pm KST

Korea Times

Top mortgage rates climb to 7.3%, highest since October 2022

주택담보대출 금리, 7.3%로 2022년 10월 이후 최고치 기록

Expectations of imminent interest rate hikes by the Bank of Korea (BOK) are adding to pressure on households and businesses already struggling with rising borrowing costs, analysts said Sunday.

한국은행의 금리 인상이 임박했다는 전망이 가계와 기업의 금리 인상 부담을 더욱 가중시키고 있다고 분석가들이 일요일 밝혔다.

Lending rates at major banks have continued to climb as BOK Gov. Shin Hyun-song struck a hawkish tone following a Monetary Policy Board meeting on May 28, reinforcing market expectations that the central bank could begin raising rates as early as July.

신현송 한국은행 총재가 5월 28일 통화정책회의 후 매파적인 기조를 보이면서 주요 은행들의 대출 금리가 지속적으로 상승하고 있으며, 이는 한국은행이 이르면 7월부터 금리 인상을 시작할 수 있다는 시장의 기대감을 높이고 있다.

According to banking industry data, fixed-rate mortgage loans offered by the country's five major lenders — KB Kookmin, Shinhan, Hana, Woori and NH NongHyup — carried interest rates ranging from 4.39 percent to 7.33 percent as of Friday.

은행업계 자료에 따르면, KB국민은행, 신한은행, 하나은행, 우리은행, NH농협 등 국내 5대 은행의 고정금리 주택담보대출 금리는 금요일 기준 4.39%에서 7.33% 사이였다.

The upper end of the range was up 0.33 percentage point from a month earlier, when rates stood between 4.4 percent and 7 percent.

이는 한 달 전 4.4%~7%였던 금리보다 0.33%포인트 상승한 수치이다.

It marked the first time since October 2022 that the highest fixed mortgage rate among the five major lenders exceeded 7.3 percent.

이는 5대 은행의 최고 고정금리 주택담보대출 금리가 2022년 10월 이후 처음으로 7.3%를 넘어선 것이다.

Personal credit loan rates have also moved higher.

개인 신용대출 금리도 상승했다.

As of Friday, interest rates on personal credit loans for top-tier borrowers with one-year maturities ranged from 4.31 percent to 5.93 percent, with the upper end nearing the 6 percent mark.

금요일 기준, 신용등급이 높은 고객을 대상으로 하는 1년 만기 개인 신용대출 금리는 4.31%에서 5.93% 사이였으며, 최고 금리는 6%에 근접했다.

The rise in market interest rates comes as investors increasingly expect the central bank to begin raising its benchmark rate in the latter half of the year amid rising geopolitical tensions in the Middle East and growing inflationary pressures.

시장 금리 상승은 중동 지역의 지정학적 긴장 고조와 인플레이션 압력 심화 속에서 한국은행이 하반기에 기준금리 인상을 시작할 것이라는 투자자들의 기대감이 커지고 있는 가운데 나타났다.

Though the BOK's Monetary Policy Board kept its benchmark rate unchanged at 2.5 percent at its May meeting, markets took Shin's remarks as a signal that a rate hike could come as early as July.

한국은행 통화정책위원회는 5월 회의에서 기준금리를 2.5%로 동결했지만, 시장은 신현송 총재의 발언을 7월 초 금리 인상 가능성을 시사하는 신호로 해석했다.

"The policy direction is relatively clear when looking at inflation, growth, the exchange rate and the housing market. Raising the benchmark rate going forward could provide an opportunity to manage these factors in a more consistent manner," Shin said during a press conference after the meeting.

신 총재는 회의 후 기자회견에서 "인플레이션, 경제 성장률, 환율, 주택 시장 등을 고려할 때 정책 방향은 비교적 명확하다. 향후 기준금리 인상은 이러한 요소들을 보다 일관성 있게 관리할 수 있는 기회를 제공할 수 있다"고 말했다.

Analysts warn that borrowing costs could rise further if the BOK enters a rate hike cycle, placing additional strain on financially vulnerable households already burdened by debt.

일각에서는 한국은행이 금리 인상 사이클에 돌입할 경우 대출 비용이 더욱 상승하여 이미 부채 부담에 시달리는 취약 가계에 추가적인 부담을 줄 수 있다고 경고한다.

"A higher policy rate will be transmitted quickly to commercial bank lending rates, putting significant pressure on heavily indebted borrowers. Financially vulnerable borrowers are likely to be hit hardest if rates continue to rise," said Kim Dae-jong, a professor of business administration at Sejong University.

세종대학교 경영학과 김대종 교수는 "정책금리 인상은 시중은행 대출금리에 빠르게 반영되어 부채가 많은 차입자들에게 상당한 부담을 줄 것"이라며, "금리가 계속 오를 경우 재정적으로 취약한 차입자들이 가장 큰 타격을 입을 가능성이 높다"고 말했다.

Small and medium-sized enterprises are also expected to face mounting pressure if the BOK begins raising interest rates, Kim said, as higher borrowing costs could weigh on firms that rely heavily on loans for funding.

김 교수는 또한 한국은행이 금리 인상을 단행할 경우 차입 비용이 증가하면서 자금 조달을 위해 대출에 크게 의존하는 중소기업들이 더욱 압박을 받을 것으로 예상된다고 덧붙였다.

Analysts also voiced concerns about the growing use of borrowed money in the stock market, warning that higher interest rates could increase repayment burdens for retail investors who have taken on debt to chase recent gains.

분석가들은 주식시장에서 차입금 사용이 증가하는 추세에 대해서도 우려를 표명하며, 금리 인상이 최근 상승세를 쫓아 차입을 한 개인 투자자들의 상환 부담을 가중시킬 수 있다고 경고했다.

The benchmark KOSPI has gained nearly 90 percent so far this year on the back of a semiconductor supercycle, fueling a sharp increase in margin borrowing among retail investors. According to the Korea Financial Investment Association, outstanding margin loans used for stock purchases surpassed 38 trillion won ($24.3 billion) for the first time as of May 29.

코스피 지수는 반도체 슈퍼사이클에 힘입어 올해 들어 약 90% 상승했으며, 이는 개인 투자자들의 마진 대출 급증을 부추겼다. 한국금융투자협회에 따르면 5월 29일 기준 주식 매수에 사용된 마진 대출 잔액이 사상 처음으로 38조 원(243억 달러)을 넘어섰다.

With margin debt at record levels, heightened market volatility could leave heavily leveraged investors increasingly vulnerable, experts said.

전문가들은 마진 부채가 사상 최고치를 기록한 가운데 시장 변동성이 커지면서 레버리지를 과도하게 사용한 투자자들이 더욱 취약해질 수 있다고 말했다.

#Interest rate hike expectations 금리인상기대 #Mortgage rates surge 주택담보대출금리급등 #Hawkish stance 매파적기조 #Household debt burden 가계부채 부담 #Margin loans expansion 마진대출 증가